MD Case Study – Countertop Manufacturer and Installer

MD Tax Assessment Amount – $113,011.03

Reduction Amount – $69,836.18 – 62%

Approved Credit/Refund – $17,335.29

Interest and Penalty Savings – $42,698.94

Maryland countertop manufacturer and installer was selected by the Comptroller’s Office for a Maryland sales and use tax audit. Taxpayer manufactured and installed countertops for residential and commercial customers in DC, MD, and VA. This Taxpayer had never been audited before and Marsu was recommended by the Taxpayer’s lawyer to assist in the audit process. Unfortunately, Marsu was not contacted in time to review the workpapers in the field with the auditor so the lawyer had to request an informal hearing and Marsu had to present the documentation to a hearing officer. The Taxpayer had been assessed tax on sales for failure to collect sales tax on commercial jobs and for failure to remit use tax on expenses and capital assets. Marsu assisted the Taxpayer in reviewing each schedule as follows:

- For sales, the auditor reviewed nine months of sales invoices and listed only 14 invoices as taxable, but the projected liability was $77,663.09. Marsu pulled the job folders to review each job and was able to document that 1 job was non-taxable, reduce the liability for 3 jobs and got the Comptroller’s Office to tax 2 jobs on an actual basis. These adjustments reduced the tax assessed from $77,633.09 to $25,496.05, a savings of $52,137.04.

- For COGS expenses, the auditor reviewed twelve months of invoices and listed 301 invoices as taxable. Marsu reviewed each line item and provided documentation to have 142 lines deleted and 2 lines reduced. These adjustments reduced the tax assessed from $24,908.39 to $14,924.70, a savings of $9,983.69.

- For assets, the auditor reviewed every asset purchased during the assessment period and listed 14 invoices. Marsu reviewed each of the assets and was able to provide documentation to get 3 of the lines deleted. The tax due was reduced from $10,469.55 to $2,754.10, a savings of $7,715.45.

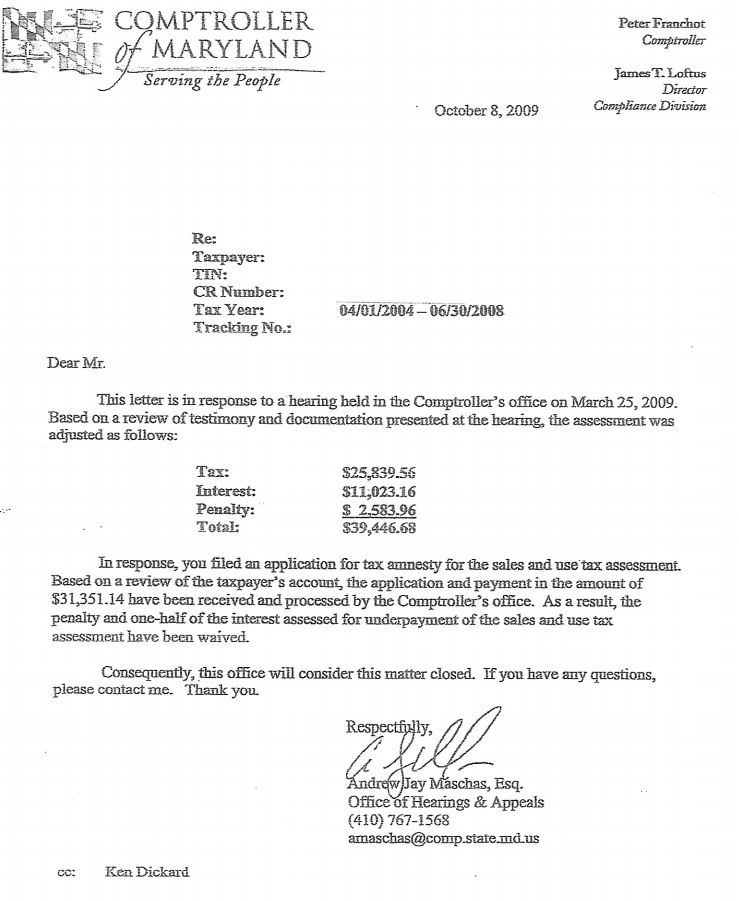

Marsu also performed a reverse audit and documented sales taxes paid in error and the Comptroller’s Office approved and included refunds in the amount of $17,335.29 in the audit workpapers as required by law. At the time of the audit, the Comptroller’s Office was offering an Amnesty Program and the Taxpayer enrolled and was able to pay only half the interest due and have the penalty abated.

Main Audit Issues

Countertop manufacturers and installers have been a favorite audit target of the Comptroller’s Office for many years. If the Taxpayer is not properly collecting tax, then the tax assessment will be in the tens of thousands or even in the hundreds of thousands of dollars depending on the size of the company and type of work performed. As you can see from this case, this Taxpayer is a testimonial to that fact. This Taxpayer did a fair amount of commercial work and was not collecting sales tax.

Twenty years or so ago, the Comptroller’s Office added the infamous two sentences to Maryland Tax Regulation .19 – Real Property Construction, Improvement, Alteration and Repair that sums up their position on taxability when auditing a countertop manufacturer and installer. “As a general rule, counters, countertops, and cabinetry installed in commercial spaces will be treated as tangible personal property. Doors, windows, molding, built-ins, and kitchen cabinetry installed in residential and commercial spaces will be treaty as realty”. So if a Taxpayer does commercial work and it is not in a kitchen or bathroom, then the Comptroller’s position is that the job is taxable and will assess the Taxpayer for failure to collect tax unless tax was collected by the Taxpayer.

So if you the Taxpayer furnish and install any of the following for a commercial business, then tax should be collected from the customer – any countertop and cabinetry installed in a non-kitchen or non-bathroom area. Examples are bank teller stations, bars, beverage counters, food stations and wine racks in restaurants, built-in shoe racks, cashier counters, lockers, reception desks, and service desk and counters. Other examples include countertops and cabinetry in all non-kitchen and non-bathroom areas in office buildings, like in copy or conference rooms. The Comptroller’s Office in this case even assessed a stone countertop ledge and cabinetry that was installed in the conference room underneath the windows even though the ledge and cabinetry was installed to bare stud walls and an operating table in a veterinarian’s office.

How Audits Happen

This audit represents a typical way that a Taxpayer gets selected for a sales tax audit. The Taxpayer’s customer gets audited first and the auditor sees that the countertop manufacturer is not collecting sales tax, so the auditor turns in the Taxpayer for an audit.

Call Marsu

Countertop manufacturers and installers are one of the most often audited types of businesses. That is because the MD sales tax law is so confusing and there are so little guidelines available. If you are a countertop manufacturer and installer and have been audited in the past, then please call Marsu now to determine if your case can be reopened pursuant to Section 13-509 of the Annotated Code of Maryland to get any taxes improperly assessed back as a refund or if you are just due a refund of sales and use taxes paid in error. Marsu’s review is performed on a contingent basis and no fee is due if no refund is approved by the Comptroller’s Office.

Click Here or Image Below for Full Letter