MD Case Study – Sales and Use Taxes – Manufacturer and Government Contractor

MD Tax Assessment Amount – $182,874.59

Reduction Amount $114,768.59 – 63%

Refund from Reverse Audit – $907,177.37

Refund from Taxpayer – $237,198.19

Interest & Penalty Savings – $73,149.84

Exceptionally large Maryland manufacturer and government contractor who manufacturers products and provides services to the federal government and has locations throughout the United States was selected for another sales and use tax audit. This Taxpayer was last audited in 2001 and Marsu assisted in that audit and had filed and gotten refunds approved by the Comptroller. Taxpayer had received their audit workpapers and was working on filing their own refunds but wanted assistance with reviewing the audit and in filing any additional refunds. Marsu assisted the Taxpayer as follows with the asset and expense schedules:

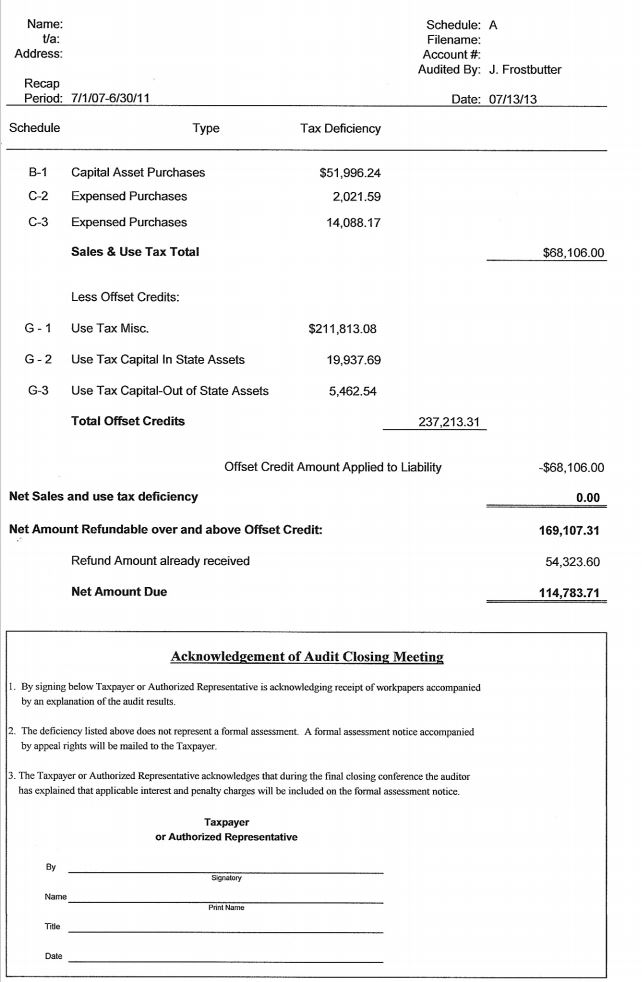

- For capital assets, the auditor reviewed all Maryland assets and listed 107 invoices as taxable. Marsu reviewed each invoice to determine where and how each asset was used to establish if an exemption was available or if sales or use tax was paid. Marsu was able to document 48 invoices were non-taxable. The tax assessed was reduced from $83,751.76 to $51,996.24, a savings of $31,755.52.

- For expenses, the auditor reviewed a one-month sample period and listed 38 invoices as taxable. Marsu reviewed each invoice and was able to get only 11 invoices deleted, but these 11 invoices represented 84% of the sample dollars. The tax assessed was reduced from $99,122.83 to $16,109.73, a savings of $83,012.60.

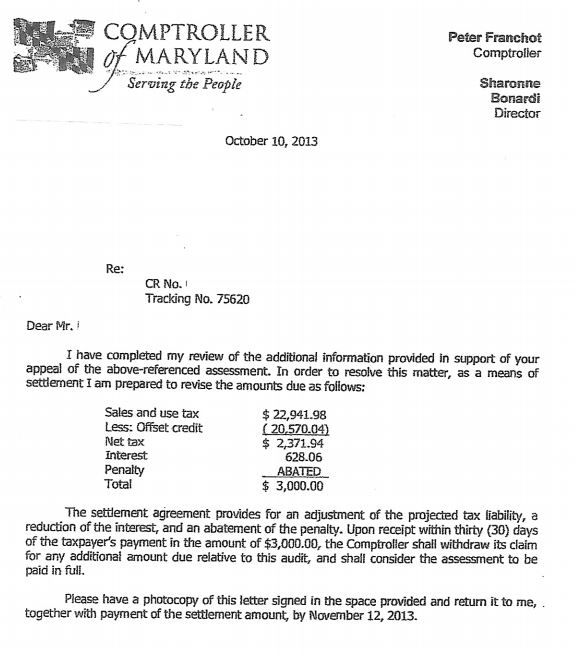

With Marsu’s assistance, this Taxapayer was able to significantly reduce their tax assessment and to recover all sales and use taxes paid in error. The original workpapers had the Taxpayer owing $182,874.59 in taxes and the final workpapers had the Taxpayer receiving refund checks in the total amount of $1,076,284.68, a savings of $1,259,159.27. Since the Taxpayer had filed their own refunds that exceeded the tax assessment amount, there was no interest and penalty assessed. This saved the Taxpayer approximately $73,149.84 in interest and penalty because the refunds were filed.

Main Audit Issues

The only minor audit issue here is that the Taxpayer sometimes misses paying use tax on some of its assets and expense items. Their percentage of error is exceedingly small. For assets, there were 6,041 assets and tax was not properly paid on 59 of them for an error rate of less than 1% – .0097665. I think that is a pretty great job. For expenses, the assessment ended up to total $16,109.76 which is a monthly average of $335.62 which is not terrible for the size of the company. A review of the final 27 invoices on the expense schedule shows that the assessment came from mainly office supplies and online purchases. One area that the States love to audit, and Taxpayers have difficulty with is credit card transactions. Usually the monthly credit card transactions are not reviewed by the Taxpayer to pay use tax and a lot of times these transactions come from out of state transactions where MD sales tax is not collected.

Audits of Exceptionally Large Businesses

Auditing exceptionally large businesses for sales and use taxes is very time-consuming job not only because of the sheer volume of records, but also because of the different exemptions or exclusions available for businesses that operate in and have contracts in multiple states. Just for the asset portion of this audit alone, this Taxpayer had to at least provide invoice copies of over 6,000 assets for the auditor to review to establish minimally that sales or use tax was paid so the asset would not be assessed. This does not even count the expense audit and heaven forbid if the Taxpayer had taxable sales and the auditor would have to review at least a one-month sample.

Time is one of the things that the States have as an advantage over the Taxpayer. The State’s auditor does not have a time limit or a job profit and loss statement to answer to. When the auditor does their audit, they will list everything possible on the workpapers and hope it sticks. If the Taxpayer does not invest the time by providing the requested information and then thoroughly reviewing the workpapers to provide additional information, then the Taxpayer will be over assessed. That is why is it is beneficial to bring in experts who for 40 years have been reviewing workpapers and dealing with auditors, supervisors, and hearing officers. Plus any refund that Marsu gets approved will offset any taxes due and decrease the interest and penalty due. After the audit is finalized, Marsu will review with the Taxapayer the refund that was approved so the Taxpayer can implement changes to their accounting system to take advantage of the annual tax savings.

Call Marsu

If you are a Government Contractor or a multi-state contractor and have been audited in the past, then please call Marsu now to determine if your case can be reopened pursuant to Section 13-509 of the Annotated Code of Maryland to get any taxes improperly assessed back as a refund or if you are just due a refund of sales and use taxes paid in error. Marsu’s review is performed on a contingent basis and no fee is due if no refund is approved by the Comptroller’s Office.

Click Here or Image Below for Full Letter