Maryland HVAC contractor working in DC, MD and VA was assessed by the DC Office of Tax and Revenue for failure to collect sales tax on taxable sales and services. After receiving the initial workpapers assessing the business $35,807.43 in taxes, the Taxpayer contacted Marsu to review the workpapers to determine if the assessment could be reduced. The taxpayer’s business is located in Maryland, but failed to properly register in DC for the collection of DC sales tax, so the statute of limitation for the audit was extended back beyond the normal three year audit period. Luckily the Taxpayer just started his business in 2015, so the starting period of the audit was 2015. Marsu assisted the Taxpayer with reviewing the sales schedule as follows:

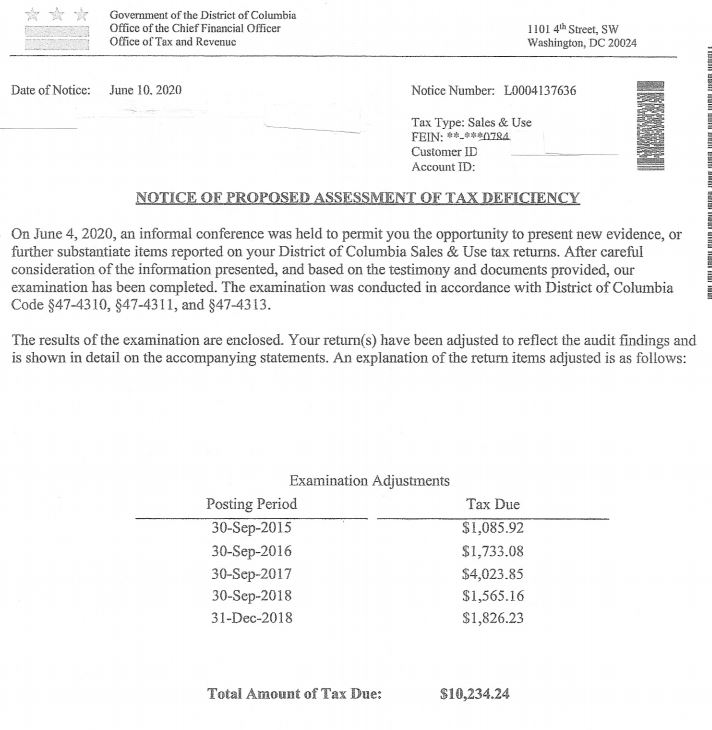

For sales, the auditor did an actual audit and reviewed all DC sales invoices for the audit period and listed 70 invoices as taxable. Marsu reviewed each invoice and proposal and documented that 19 invoices were not taxable and that 14 invoices were reduced. The tax assessed was reduced from $35,807.43 to $10,234.24, a savings of $25,573.19.

For expenses, after Marsu provided documentation that some of the sales were actually for furnishing and installing equipment deemed real property after installation, the hearing officer requested that the Taxpayer prove that sales tax was properly paid on the materials incorporated into those jobs. Marsu provided the material invoices for each job to document that sales tax was properly paid on all materials to the suppliers and no further tax was due.

Upon getting the workpapers from the Taxpayer, Marsu contacted the auditor and supervisor to see if the workpapers could be reviewed in the field, but the supervisor stated that an informal conference would have to be requested. Marsu requested an informal conference and Marsu provided the above mentioned documentation and the total assessment, including penalty and interest, was reduced from the $56,042.04 to $16,721.14, a savings of $39,320.90. Marsu was also able to get the penalty cut in half by the supervisor and filed a Maryland sales tax refund in the amount of $7,691.40.

Main Audit Issue

In DC, there is a big difference is the sales tax laws regarding real property contractors who furnish and install, repair or alter equipment into real property in DC vs MD and VA. Certain services for HVAC contractors, like maintenance contracts and T&M billings for repair of real property are taxable services and tax should be collected from the customer. Effective July 1, 1989, DC amended their sales tax law to include the T&M billing as a taxable service where sales tax is to be collected on only the material portion of the bill. As mentioned above, the Taxpayer failed to register to collect DC sales tax and was held liable for the tax that the Taxpayer did not collect. Like many audits, this Taxpayer’s audit arose from the audit of one of his customers where the auditor saw that the Taxpayer was not collecting tax.

Please see section on website on DC Real Property Services that are taxable for other services that are taxable besides maintenance agreements and T&M billings.

Other DC Concerns

The normal statute of limitations for a DC sales tax audit is three years, but DC’s policy is that if the Taxpayer should have been licensed to collect tax, but does not get licensed, then DC is allowed to extend the audit back as far as it wants. As mentioned above, the Taxpayer had just started his business in 2015 so the audit period was for a five year period.

DC Tax Assessment Amount – $113,149.05

Reduction Amount – $54,411.35 – 48%

DC and MD Sales and Use Tax Refunds – $26,042.91

Maryland elevator contractor working in DC, MD and VA was assessed by the DC Office of Tax and Revenue for failure to collect sales tax on elevator maintenance agreements. Marsu was contacted by the Taxpayer’s lawyer to review the workpapers to determine if the assessment could be reduced. The taxpayer’s business is located in Maryland, but failed to properly register in DC for the collection of DC sales tax, so the statute of limitation for the audit was extended back beyond the normal three year audit period. The assessment period ended up to be for six years and four months. Marsu did the following for the sales schedule in the audit:

For sales, the auditor reviewed the calendar year 2009 as a sample period and listed all the maintenance contracts by customer total. The sales schedule had totals for 56 DC customers who had maintenance contracts. Marsu reviewed each customer and was able to delete 20 customers from the list. The taxable sales for the sample period was reduced from $682,754.78 to $360,209.10 and the error factor was reduced from 11.8799% to 6.1671%, a reduction of 48%. This error factor was then applied to all maintenance contracts in the audit period to calculate the taxable maintenance agreement basis for each year and then that basis was multiplied by the applicable tax rate to obtain the tax assessment due.

After reviewing the DC audit workpapers, Marsu performed a reverse audit and was able to secure refunds for DC and MD in the amount of $26,042.91. These refunds assisted the Taxpayer in paying their liability to DC and to save tax dollars for years to come.

Main Audit Issue

In DC, there is a big difference is the sales tax laws regarding real property contractors who furnish and install, repair or alter equipment into real property in DC vs MD and VA. Certain services for elevator contractors, like maintenance contracts, are taxable services and tax should be collected from their DC customers. As mentioned above, the Taxpayer failed to register to collect DC sales tax and was held liable for the tax that the Taxpayer did not collect.

Please see section on our website on DC Real Property Services that are taxable for other services that are taxable besides maintenance agreements.

Other DC Concerns

The normal statute of limitations for a DC sales tax audit is three years, but DC’s policy is that if the Taxpayer should have been licensed to collect tax, but does not get licensed, then DC is allowed to extend the audit back as far as it wants. As mentioned above, the audit period for this Taxpayer ended up being for six years and four months, over twice the normal period.

Maryland woodworking and cabinet making shop was selected by the Comptroller’s Office for a Maryland sales and use tax audit. This taxpayer had been audited before and Marsu was contacted by the Taxpayer’s lawyer to assist in the audit process. Like any other audit, the auditor reviewed a sample period of sales and expenses and projected the assessment over the audit period and reviewed all asset purchases. Marsu assisted the Taxpayer in reviewing each schedule as follows:

For sales, the auditor reviewed three months of sales invoices and listed 77 out of 223 invoices as taxable. Marsu had Taxpayer pull invoices, contracts, and job estimation sheets to prove to the auditor that an invoice was not taxable. Sales schedule ended up with just 8 taxable invoices where tax was not properly collected. The tax assessed was reduced from $54,939.82 to $24,488.35, a savings of $30,451.47.

For sales tax projection methodology, the Comptroller’s methodology did not fairly represent the Taxpayer’s business over the audit period so Marsu had the Taxpayer document an alternative methodology that was accepted by the Comptroller’s Office. Alternative methodology saved the Taxpayer approximately $10,000 in tax on the sales schedule.

For expenses, the auditor reviewed three months of expense invoices and listed 188 invoices as taxable. Marsu reviewed each line item and provided documentation to the auditor that the line was not taxable or that use tax was paid. The expense schedule was reduced by 67% of the dollar value of the invoices listed. The Taxpayer had a complicated system of paying use tax and showing that the purchase was for resale. The Comptroller made the Taxpayer prove each line item that was for resale by matching the purchase to its’ corresponding sales invoice. This was a very time-consuming process. The tax assessed was reduced from $78,406.27 to 23,945.91, a savings of $54,460.36.

For assets, the auditor reviewed every asset purchased during the audit period and only found issue with one invoice. Marsu agree that the one invoice was taxable.

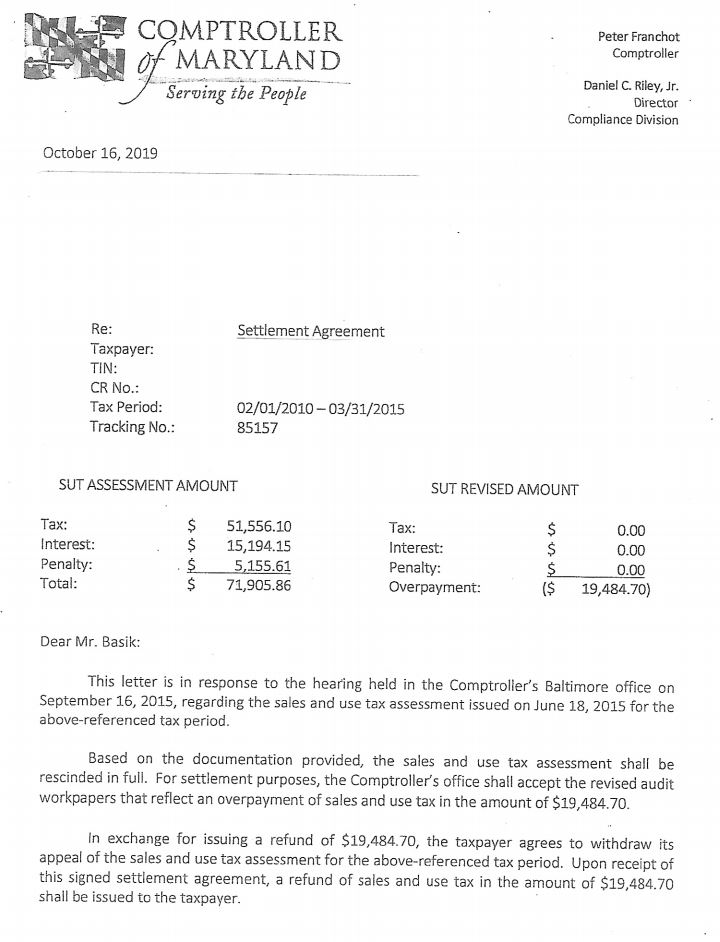

Marsu also performed a reverse audit and documented sales and use taxes paid in error and the Comptroller’s Office approved and included the refund in the amount of $73,202.29 in the audit workpapers as required by law. The original workpapers had the Taxpayer owing $138,629.42 in taxes and the final workpapers had the Taxpayer receiving a refund check in the amount of $19,484.70, a savings of $158,114.12. Since the Taxpayer received a refund, there was no interest and penalty assessed.

Main Audit Issues

Cabinet and countertop manufacturers have been a favorite audit target of the Comptroller’s Office for years. If a Taxpayer is not collecting tax properly, then the assessment will be in the tens of thousands of dollars or even hundreds of thousands of dollars depending on the size of the company and type of work performed.

Twenty years or so ago, the Comptroller’s Office added the infamous two sentences to Maryland Tax Regulation .19C(5) – Real Property Construction, Improvement, Alteration and Repair that sums up the Comptroller’s position of taxability when auditing a cabinet and countertop installer. “As a general rule, counters, countertops, and cabinetry installed in commercial spaces will be treated as tangible personal property. Doors, windows, molding, built-ins, and kitchen cabinetry installed in residential or commercial spaces will be treated as realty”. So if a Taxpayer does commercial work and it is not in a kitchen or bathroom, then the Comptroller’s Office is going to assess the Taxpayer regardless of how the cabinetry or countertop is installed. Even commercial built-in cabinetry work that is installed directly against wall studs or recessed into the wall is considered tangible by the Comptroller’s Office. For the Comptroller’s Office the word built-ins are defined as like garbage disposals not built-ins as understood by the cabinetry manufacturers and installers.

So if you furnish and install any of the following, then tax should be collected from the customer – any cabinetry and countertop installed in a non-kitchen or bathroom area, like in a doctor’s office or a work area room (paper copy station), bank teller stations, bars and food stations in restaurants, benches, cashier counters, concession stands, credenzas, lockers, reception desks, and service desks and counters. The Comptroller has even assessed window ledge under windows in conference rooms, recess cabinetry in walls, and sinks in common areas of doctor’s office or exam rooms.

One minor issue in the sales tax collection area was fabrication labor. If the Taxpayer takes the customer’s material and manufacturers an item or just performs a simple task as cutting or drilling holes in the material, then the Taxpayer’s labor charge is taxable. The Comptroller’s Office considers the labor as part of taxable price of the finished product. Just because the labor to manufacture a product is performed by two or more businesses, it is still taxable. If one Taxpayer had performed all the labor to manufacture a product, then the total price is taxable. See MD Tax Regulation 30 – Fabrication or Production for the Comptroller’s description of what fabrication labor is.

The last major issue in this audit was inventory items used in jobs for resale and also in jobs where the Taxpayer is installing the material into real property. If the material is used in a job for resale, then no tax is due on the material when purchased and tax is collected from the customer on that material. If the material is used by the Taxpayer on a real property job that is installed by the Taxpayer, then tax is due on the cost of the material incorporated into the job. Taxpayer was buying all the inventory items for resale and paying no use tax when used on realty jobs. Inventory items were items like bolts, caulk, glue, hardwoods, melamine, molding, nails, paint, plywood, screws, shims, stain, thinner and washers. Problem was that items purchased in bulk were not allocated to realty or resale jobs, so the Taxpayer had no methodology to self-assess use tax on the material cost of inventory items being used in realty jobs. The Comptroller’s Office took the position that 100% of the inventory items were taxable. For the hardwoods purchased by the Taxpayer, Marsu matched the purchase to sale invoices to get the purchase removed or reduced on the expense schedule. For all the other items, Marsu calculated a percentage of sales dollars of non-taxable jobs to total jobs for the sales sample period and used that percentage to reduce the inventory items on the expense schedule. The Comptroller’s Office accepted this analysis.

Call Marsu

Countertop manufacturers and installers are one of the most often audited types of businesses. That is because the MD sales tax law is so confusing and there are so little guidelines available. If you are a countertop manufacturer and installer and have been audited in the past, then please callMarsu now to determine if your case can be reopened pursuant to Section 13-509 of the Annotated Code of Maryland to get any taxes improperly assessed back as a refund or if you are just due a refund of sales and use taxes paid in error. Marsu’s review is performed on a contingent basis and no fee is due if no refund is approved by the Comptroller’s Office.

Maryland golf course was selected by the Comptroller’s Office for a Maryland sales and use tax and admissions and amusement tax audit. This taxpayer had been audited before for sales and use tax, but this time the audit was trigger by non-payment of admissions and amusement taxes. The number one issue that triggers an audit more than anything else is failure to file returns. Marsu was contacted by the Taxpayer’s lawyer to review the completed workpapers. Taxpayer had calculated the amount of admissions and amusement taxes that were due and submitted a check prior to the audit workpapers being finalized. I am assuming the Taxpayer did this to stop interest from accruing. Since the Taxpayer had received their Notice of Assessment, the case could not be reviewed in the field, so the lawyer filed for an informal hearing. Marsu did the following for the asset, sales, expenses and lease audit schedules for the sales tax audit and the admissions and amusement calculation schedule for the admissions and amusement tax audit:

The auditor reviewed every asset purchased during the audit period and only listed 7 invoices. Marsu was able to obtain a copy of one (1) of the invoices to prove that sales tax had been paid to the supplier. The tax assessed was reduced from $2,007.56 to $1,932.39, a savings of $75.17.

For expenses, the auditor reviewed a three month sample period and listed 38 invoices. Marsu reviewed each line item and provided documentation to the hearing officer to get 15 lines deleted from the workpapers. Documentation included contracts, account number information and copies of invoices. The tax assessed was reduced from $14,126.08 to $5,398.20, a savings of $8,727.88.

For lease schedule, the auditor reviewed all leases and listed two (2) leases. Marsu presented copies of invoices from one of the leases where sales tax was paid. The tax was reduced from $18,062.85 to $13,424.64, a savings of $4,638.21.

For sales, the auditor listed the revenue from the accounts that were taxable for the audit period on a yearly basis and totaled all taxable sales and subtracted the sales tax remitted to calculate the tax assessment. Since alcohol sales were involved, there was a 6% and 9% tax assessment schedules. Marsu reviewed these schedules and determined that not all the proper accounts were included and not all the sales were taxable sales. Marsu documented the additional accounts and the non-taxable sales to the hearing officer and the schedules were reduced. The 6% schedule was reduced from $18,062.85 to a refund of $13,544.42, a savings of $31,607.27. The 9% schedule was reduced from $2,413.37 to a refund of $10,710.04, a savings of $13,123.41.

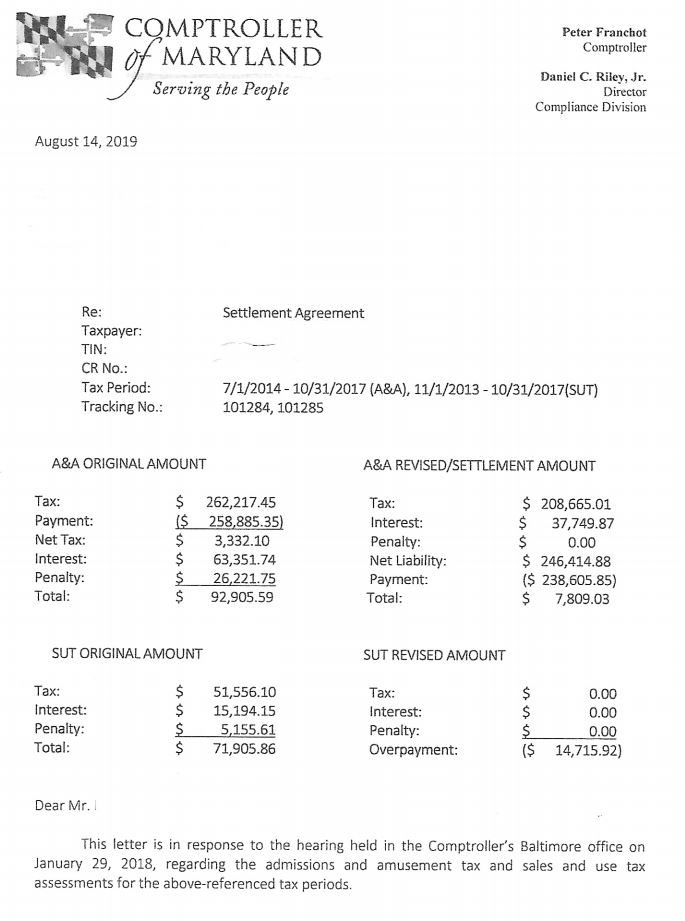

For admissions and amusement taxes, the auditor listed the revenue accounts that were taxable for the period to calculate the 10% tax that was due. Marsu reviewed this calculation and determined that not all sales were taxable and then provided documentation for those non-taxable sales to the hearing officer. The tax was reduced from $262,217.45 to $208,665.01, a savings of $53,552.44.

Main Audit Issues

Over the years, Marsu has reviewed several audits of golf courses for sales taxes. I believe they are a favorite target of the Comptroller’s Office because they are auditing for two taxes at one time, for sales taxes they are auditing that the 6% and 9% tax is collected properly, and that the industry purchases a lot of equipment from out of state suppliers and use tax is not always paid.

The first issue here was that the Taxpayer was not filing their admissions and amusement tax returns. That is a red flag for the Comptroller’s Office and they will always perform an audit to get their money. Taxpayers should always file tax returns and pay timely so you do not attract attention to themselves and get audited.

The second issue was that the Taxpayer was not paying any use tax. This was at least the second audit for sales and use taxes and re-audits is one area that the Comptroller’s Office obtains audit candidates from. The Comptroller’s Office will review the payment history of Taxpayers who were audited in the past ten years or so and had large assessments. A certain percentage of them will be selected for a re-audit to confirm that the Taxpayers made changes from their last audit to be in better compliance with collecting and paying use tax.

Maryland electrical contractor was assessed for failure to collect sales tax for the period of November 2009 through May 2015. The assessment period of five years and six months seems to be a little longer than normal. The Taxpayer told me that the audit was transferred from one auditor to another till it was completed and that is why it took so long to complete. The Taxpayer was assessed $132,652.42 in taxes in 2015 and now owes over $260,000.00. Marsu was contacted by the Taxpayer in October 2018 to determine if they could be of any assistance. Marsu reviewed the case and determined that the Taxpayer was a consuming contractor and not a retailer, so no sales tax needed to be collected from the Taxpayers’ customers. Marsu did the following for the sales schedule of the audit:

For sales, the auditor reviewed three months of invoices and listed 13 transactions on the sales schedule which constituted all the revenue transactions for the period. Transactions were actually payments for subcontract work for a related company. Marsu had the Taxpayer document the detail of the four transactions that were all labor separate from the nine transactions that were for the furnishing and installing of equipment that after installation was deemed to be real property.

After the Comptroller’s Office agreed that the equipment was real property after installation, Marsu had to prove that sales tax was properly paid on the equipment installed. Marsu supplied copies of the equipment invoices and payment checks to document that sales tax was properly paid to the supplier.

Marsu supplied the above documentation to the Comptroller’s Office and after their review, the Comptroller agreed with my position that the labor was a non-taxable transaction and that the equipment did become real property after installation. The original tax assessment of $132,652.42 plus all penalties and interest was abated in full. There was also a small issue with payment of sales and withholding taxes that was cleared up and the Taxpayer’s Statement of Account was reduced from $4,715.49 to $0.00, an additional savings of $4,715.49.

Main Audit Issues

From the hearing officer’s letter, the taxpayer did not file a timely appeal, but under Section 13-509 of the Tax-General Article, the Comptroller’s Office can open up a case to correct an erroneous final assessment. The Comptroller did open up the case and the Taxpayer provided documentation and it seems that the Comptroller and the Taxpayer went back and forth with documentation requests and extensions with no adjustments being made to the assessment. Undoubtedly the Taxpayer did not present the documentation in a manner that showed that the sales under audit was subcontract work for a related company, that the work was realty work and that sales tax was paid on all materials incorporated into the job. If the Taxpayer had done so, then the assessment would have been abated in full as Marsu was able to do.

Like many cases, this was a first-time audit of the Taxpayer and the Taxpayer tried to handle the audit on their own which now is easy to see was a big mistake. From the audit workpapers, I know that the Taxpayer provided expense invoices and sales amounts for the sample periods requested but have no idea what was provided in regard to what the sales were for. I know the auditors knew that if the equipment were furnished and installed that the equipment would be deemed real property. So I am at a loss as to why this case got so far for so long. Not sure if the problem had to do with having multiple auditors or with inexperienced auditors. Most likely, there was a communication gap between the Taxpayer and the auditors and supervisors. The auditors did not ask the right questions to determine exactly what the 13 transactions were on the sales schedule and probably presumed from the Taxpayer’s website that they were making retail sales of equipment, and the Taxpayer did not know the sales tax law for retail sales vs. furnishing and installing equipment into real property. Glad the case got resolved in favor for the Taxpayer, but sad to see the Taxpayer had to go through hell and back to get there.

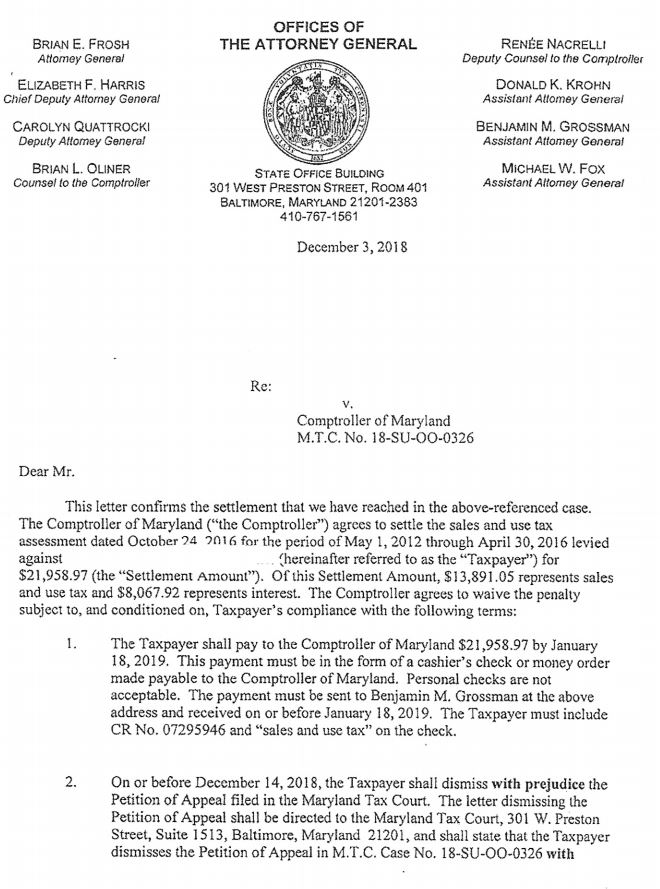

Maryland Taxpayer provides security guard and private investigative services to private, government and other clientele. Taxpayer was selected by the Comptroller’s Office for a Maryland sales and use tax audit. Taxpayer went through the audit process himself and went to an informal hearing without getting any relief from the $36,291.73 tax liability. Marsu was contacted by the Taxpayer’s lawyer to review the workpapers to determine if any adjustments could be requested. Taxpayer was being assessed for failure to collect sales tax on all line items on their invoices for security and private investigative services, failure to pay use tax and failure to remit all sales taxes collected. Since the Taxpayer had already had an informal hearing, the lawyer had to file an appeal to the Maryland Tax Court and then present our finding to the Maryland Attorney General’s Office for any reductions. Marsu did the following for each of the schedules:

For taxes collected but not remitted, the auditor did an analysis comparing the MD sales tax collected, monthly sales tax liability report and the tax remitted to come up with the liability which was almost half the assessed tax amount for the whole audit. Marsu reviewed this schedule and found that the auditor had incorrectly recorded the tax collected amount for four of the months and tax liability became zero. The tax assessed was reduced from $15,915.00 to $0, a savings of $15,915.00.

For sales, the auditor reviewed six months of invoices and listed 87 lines on the workpapers. Marsu reviewed the 87 lines and only found two adjustments. Marsu also reviewed the projection methodology and found that the total sales for the oldest year should have been for only 8 months and not for the entire year as the Comptroller had recorded. Marsu also found that the total sales for the sample period was higher than recorded. With these four minor adjustments, the liability for failure to collect sales tax was reduced from $17,378.10 to $13,492.88, a savings of $3,885.22. These four minor adjustments alone paid the bill for the lawyer and Marsu to do their review and present the case to the AG’s Office.

For expenses, the auditor again reviewed six months of invoices and listed 38 lines on the workpapers. Marsu reviewed the 38 lines and found that all lines were correct. Marsu also reviewed the expenses projection methodology and again found that the expenses for the oldest year should have been for only 8 months and not for the entire year as the Comptroller had recorded. This minor adjustment reduced the expense tax assessment by $340.48.

In the Settlement Agreement with the Attorney General’s office, the lawyer was also able to get the 10% penalty abated.

The total assessment due, including penalty and interest, in the Notice of Final Determination was $58,209.91. After our review, the Taxpayer paid, per the Attorney General’s Settlement Letter, $21,958.97, a savings of $36,259.04.

Main Audit Issue

Effective July 1, 1992, security and private investigative services in Maryland became a taxable service. Over the years, Marsu has represented several security firms and has seen plenty of firms listed in the Maryland Business Journal for liens being attached against the business for a sales tax audit. Usually these cases have assessments in the hundreds of thousands of dollars in just tax amount due. And the reason for all these tax assessments is the failure to properly collect tax on all items listed on an invoice for services provided. The Comptroller’s position is that all charges are part of the price of the services provided and taxable. So security firms should be collecting tax on all lines listed on their invoice.

Call Marsu

If you provide taxable services and want to confirm that sales tax is being properly collected, then please call Marsu to do a mock sales tax audit. See our Mock Audit Services tab on the website. State sales tax collection assessments does not only deal with getting proper resale certificates, but with collecting tax on all appropriate line items on your invoices. General rule is that all lines are taxable unless there is a specific exemption in the law.

Maryland Taxpayer who has several catering locations throughout the Baltimore Metropolitan area was selected for another sales and use and admissions and amusement tax audit. This Taxpayer was last audited in 2004 and Marsu also assisted in that audit. Taxpayer is very well versed in the proper collection of sales taxes and in the payment of use and admission and amusement taxes. The Taxpayer just received the audit workpapers for the sales and use tax audit and there was no assessment for the admissions and amusement tax audit, but the Taxpayer discovered two refunds from the admissions and amusement tax audit that they were putting together to submit to the auditor so it could be incorporated into the audit. The Taxpayer contacted Marsu to review the sales tax audit to determine what, if any, adjustments could be presented to the auditor. Marsu did the following for the asset and expense schedules:

For assets, the auditor reviewed all the asset purchases for all locations for the audit period and listed 42 invoices as taxable. Marsu reviewed each invoice and discovered that use tax had been paid on 7 of the invoices that the auditor missed in his review and 7 other invoices that were not taxable. The tax assessed was reduced from $6,945.08 to $4,069.38, a savings of $2,875.70.

For expenses, the auditor only looked at a one-month sample for all locations and listed 65 invoices as taxable. Marsu reviewed each invoice and documented that 2 invoices were non-taxable and got 3 lines deleted and assessed on an actual basis for each supplier for the audit period. The tax was reduced from $58,320.73 to $42,218.85, a savings of $16,101.88.

After the review of the workpapers, Marsu performed a reverse audit and documented sales and use tax paid in error and the Comptroller’s Office approved and included Marsu’s refund in the amount of $14,595.52 and the refunds filed by the Taxpayer in the workpapers as required by law. The original workpapers had the Taxpayer owing $65,265.81 in taxes and the final workpapers had the Taxpayer owing $0 in taxes, a savings of $65,265.81. Since the audit had a $0 amount of tax due, there was no interest and penalty due. From the original workpapers, the taxpayer saved $19,070.72 in interest because of the refunds approved from Marsu and the Taxpayer.

Collection of Tax by Caterers

This Taxpayer has been 100% compliant in the collection of sales taxes in the past two audits that Marsu has been involved in. That is a testimony to the great job that this Taxpayer is doing in this area. Caterers are to collect tax on almost every line item that is included in the bill. The main exception is the hall rental charge if separately stated. Usually most caterers do not have their computer system’s programed to collect tax on some labor or rental charges and then gets dinged for failure to collect sales tax when audited by the Comptroller’s Office.

Main Audit Issues

The only minor audit issue here is that the Taxpayer sometimes misses paying use tax on some of its assets and expense items. I mainly chalk this up to clerical errors because the Taxpayer does a decent job of paying use tax. One thing that Marsu recommends and this Taxpayer does is after an audit is to call up the MD suppliers who did not properly collect sales tax and inform them that they should be collecting tax. That way in the future the Taxpayer will be properly paying the tax to the supplier and does not have to worry about accruing use tax and possibly missing it again and it being included in the next audit. Because this Taxpayer knows they will be audited again.

The majority of the expense items included in this audit were items that were deleted in the 2004 audit because they were for resale and the Comptroller’s Hearings and Appeals section agreed. The auditor in the audit section was just following their guidelines which comes from a 2006 Maryland Tax Court Case that stated that similar items were taxable. Recently, the Comptroller’s Office has issued a Business Tax Tip that discusses the taxability of different expense items that a caterer uses to cater an event. This Tax Tip just confirmed the ruling that this Taxpayer received in their 2004 audit and has been following ever since.

Call Marsu

If you are a caterer and have been audited in the past, then please call Marsu now to determine if your case can be reopened pursuant to Section 13-509 of the Annotated Code of Maryland to get any taxes improperly assessed back as a refund or if you are just due a refund of sales and use taxes paid in error. Marsu’s review is performed on a contingent basis and no fee is due if no refund is approved by the Comptroller’s Office.

Maryland Taxpayer manufactured and installed canvas and fabric awnings and installed aluminum awnings. This was a first-time audit of the Taxpayer for sales and use taxes. Marsu was contacted by the Taxpayer’s lawyer to assist in the review of the workpapers right after receiving the initial workpapers that stated that the Taxpayer owed $254,494.80 for failure to collect sales tax on the sale of tangible personal property and to pay use tax on expenses. Marsu contacted the auditor to setup an appointment to review the workpapers. Marsu assisted the Taxpayer in reviewing the sales and expense schedules:

For sales, the auditor reviewed just a one-month sample period and listed 40 invoices as taxable. Marsu pulled the contracts and job estimation sheets for each job and documented that 4 invoices were not taxable. Marsu also reviewed the projection methodology and presented an alternative methodology that significantly reduced the sales tax projected assessment. Part of the new methodology was assessing a certain type of awning installation and assessing it on an actual basis instead of projecting. 10 invoices on the sales schedule was moved from the projection schedule to sales that were assessed on an actual basis. This methodology was accepted by the Comptroller’s Office. The tax assessed was reduced from $199,547.67 to $130,107.79, a savings of $69,439.88.

For expenses, the auditor reviewed just a one-month sample period and listed 14 invoices as taxable. Marsu reviewed the 14 invoices and documented that 8 invoices were not taxable. The tax assessed was reduced from $53,900.49 to $445.68, a savings of $53,454.81.

For sales and expenses, Marsu was also finally able to get the Comptroller’s Office to agree that a certain type of awning installation was not a sale of tangible personal property but was deemed real property after installation for residential, not commercial sales. This transaction was taken out of the original assessment with the auditor as a sale that was included in the projected sales assessment to being assessed on an actual basis and now is having all residential sales taken out. The tax assessed for Actual Sales being taxed was reduced from $57,354.78, to $2,700.36, a savings of $54,654.42. Since this item was deemed to be real property after installation, the Comptroller’s Office had Marsu perform an audit on the purchases of the real property installation item and the Taxpayer was assessed an additional $26,759.43 in tax. These taxes were assessed as Expenses – Actual in the audit workpapers.

After Marsu’s review of the workpapers with the auditor in the field, the auditor was not able to make the adjustment outlined in #3 above and some other adjustment requests, so the lawyer filed for an informal hearing. Prior to the informal hearing, Marsu has been able to get the tax assessed reduced from $254,494.80 to $131,600.11, a savings of $123,894.69.

At the informal hearing, the lawyer presented our case to the hearing officer that the Taxpayer was a real property contractor and did not sell tangible personal property. The lawyer presented two (2) miniature types of awnings that the Taxpayer manufactured and installed to provide the Comptroller’s Office a better idea of what the awning looked like and how they are manufactured and installed. The lawyer also presented literature on a third type that the Taxpayer installed. Because of the complexities of this case, our case was handed to a higher official within the Comptroller’s Office for review.

Marsu presented the case again to this third person. Marsu was able to get the Comptroller to remove the third type of awning that was presented at the hearing out of the audit for residential customers only. The Comptroller agreed that these sales to residential customers were deemed to be real property and not taxable, but sales to commercial customers were still deemed to be tangible personal property and taxable. These sales had previous been taken out of the sales projection and assessed on an actual basis. The Sales – Actual that were added to the workpapers were reduced from $57,354.78 to $2,700.36, a savings of $54,654.42. Also at this review, the Comptroller’s Office approved a refund documented by Marsu in the amount of $12,850.09. This refund was incorporated into the workpapers as required by law.

Since these sales were taken out of the audit, the Comptroller’s Office had the Taxpayer perform an audit of the materials incorporated and installed for this third type of awning to determine if sales or use tax had been paid. The Taxpayer had not paid sales tax on these materials, but occasionally had paid use tax. The self-audit determined that the Taxpayer owed $26,759.43 in use tax on these materials. Even though the Taxpayer owed this tax, the taxpayer still saved $27,894.99 in taxes on these transactions from the audit because they were moved from the sales schedule to the expense schedule.

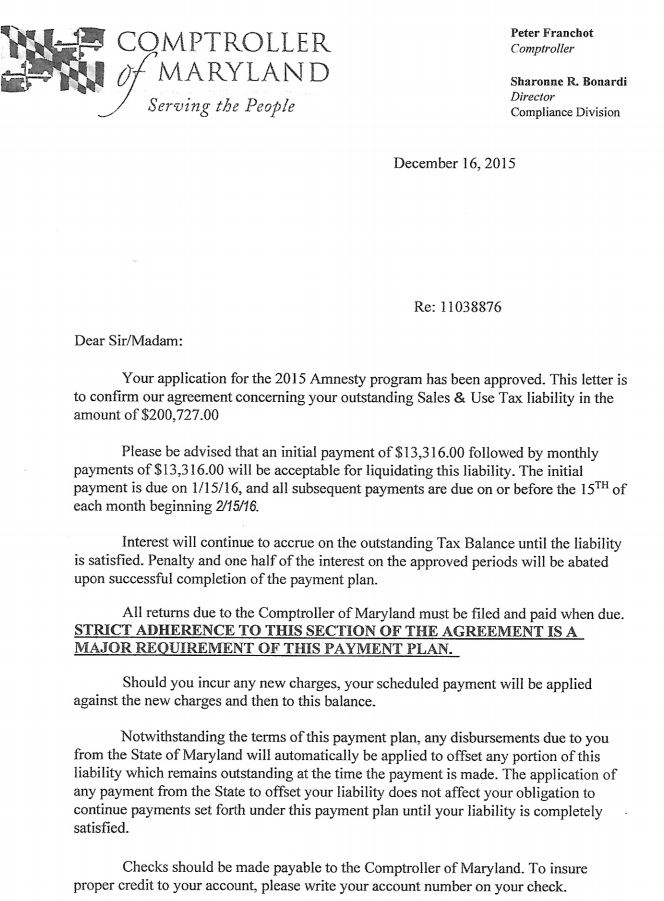

The last item that Marsu was able to do for the Taxpayer was to have them sign up for the 2015 Tax Amnesty Program. Taxpayer was approved to the program and upon full payment of the liabilities, the program abated 50% of the interest due and the 10% penalty was abated in full. See Comptroller’s Letter of December 16, 2015. By signing up for the Amnesty Program, the Taxpayer saved $25,021.48 in interest and $9,085.50 in penalty from the final assessment amount of $90,855.03.

Collection of Tax by Awning Installers

The problem in this industry is that their product, an awning, seems to be installed to improve real property because if its’ attachment to buildings or homes and for real property tax purposes is included in the real property assessment for all building or home owners. In a lot of states, awnings are deemed to be real property in their laws or regulations. But the Maryland Comptroller’s Office for sales and use taxes deem an awning as a sale of tangible personal property even though there is no public written information to that fact. The Comptroller’s Office audit department cling to some internal memo that was written in 2002 to a Taxpayer that had requested a response. Keynote … private letter. There is nothing in Maryland laws or regulations that say that awnings are tangible personal property, so the Taxpayers have no clue.

So when an awning installer gets audited, the audit department will conduct the audit and will use the 2002 letter as their documentation that awnings are tangible personal property and assess all new canvas and fabric awning installations as tangible personal property. Because of the letter, the audit department cannot audit otherwise. A Taxpayer must go further in the appeal process to possibly get tax relief.

Main Audit Issues

This is the classic case where the Taxpayer believes they are a real property contractor and has no knowledge otherwise, but when audited by the Comptroller’s Office they are deemed that some portion of their business is for the sale of tangible personal property and assessed 6% tax on those sales.

Another problem here was that the Taxpayer did not properly pay use tax on materials that were installed into real property. When being audited by the Comptroller’s Office for sales and use tax, the auditor will be auditing on two main issues. First if the Taxpayer is supposed to collect tax, then the auditor will review all sales invoices in a sample period to determine if sales tax was properly collected. And second, if the taxpayer is a real property contractor, then the auditor will be reviewing construction materials in a sample period to determine if sales tax was paid to the suppliers or use tax was self-assessed.

Call Marsu

If you are a Taxpayer who manufactures and installs awnings or just installs awnings and have been audited in the past, then please call Marsu now to determine if your case can be reopened pursuant to Section 13-509 of the Annotated Code of Maryland to get any taxes improperly assessed back as a refund or if you are just due a refund of sales and use taxes paid in error. Marsu’s review is performed on a contingent basis and no fee is due if no refund is approved by the Comptroller’s Office.

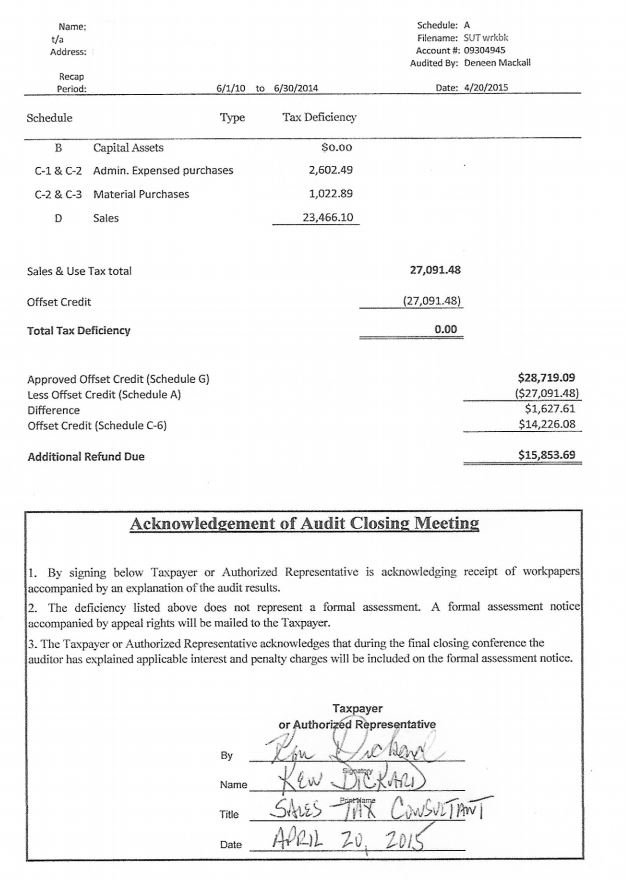

Maryland countertop manufacturer and installer was selected by the Comptroller’s Office for a Maryland sales and use tax audit. This taxpayer had never been audited before and Marsu was recommended by the Taxpayer’s accountant to assist in the audit process. Luckily, we were contacted as the initial workpapers were issued and Marsu was able to review the workpapers with the field auditor and supervisor. No informal hearing was needed. Like any other audit, the auditor reviewed a sample period of sales and expenses and projected the assessment over the audit period and reviewed all asset purchases. Marsu assisted the Taxpayer in reviewing each schedule as follows:

The auditor reviewed six months of sales invoices and listed only 7 invoices as taxable. Marsu pulled the job folders to prove to the auditor how the three invoices were not taxable. The jobs that were removed were either a residential install or for resale. The sales schedule ended up with just 4 taxable invoices where tax was not properly collected. The tax assessed was reduced from $37,202.14 to $23,466.10, a savings of $13,736.04.

The auditor reviewed three months of material (COGS) expense invoices and listed only 9 invoices as taxable. Marsu reviewed each line item and provided documentation to the auditor to have one line deleted and one line reduced. Even though Marsu only change two lines, the changes reduced the dollar value of the invoices listed by 32% and the tax due was reduced from $2,390.78 to $1,022.89, a tax savings of $1,367.89.

The auditor created a second expense schedule for administrative expenses and again reviewed six months of invoices. There were 22 lines listed. Marsu reviewed each line and was able to prove to the auditor that either tax was paid or the invoice was a non-taxable transaction for nine lines. The tax due for this schedule was reduced from $$4,390.06 to $2,602.49, a savings of $1,787.57.

The auditor reviewed every asset purchased during the audit period and the Taxpayer had properly paid sales tax to the vendor.

Marsu also performed a reverse audit and documented sales taxes paid in error and the Comptroller’s Office approved and included the refunds in the amount of $42,945.17 in the audit workpapers as required by law. The original workpapers had the Taxpayer owing $43,982.98 in taxes and the final workpapers had the Taxpayer receiving a refund check in the amount of $15,853.69, a savings of $59,836.67. Since the Taxpayer received a refund, there was no interest and penalty assessed. Without the refund, interest would have been assessed at approximately 30% and penalty at 10% to the total tax due of $27,091.48.

Main Tax Issue in Audit

Countertop manufacturers have been a favorite audit target of the Comptroller’s Office for years. If the Taxpayer is not collecting tax properly, then the assessment will be in the tens of thousands of dollars or even in hundreds of thousands of dollars depending on the size of the company and type of work performed.

Fifteen years or so ago, the Comptroller’s Office added the infamous two sentences to Maryland Tax Regulation .19 – Real Property Construction, Improvement, Alteration and Repair that sums up the Comptroller’s position of taxability when auditing a countertop installer. “As a general rule, counters, countertops, and cabinetry installed in commercial spaces will be treated as tangible personal property. Doors, windows, molding, built-ins, and kitchen cabinetry installed in residential or commercial spaces will be treated as realty”. So if a Taxpayer does commercial work and it is not in a kitchen or bathroom, then the Comptroller’s Office is going to assess the Taxpayer regardless of how the countertop is installed.

So if you furnish and install any of the following, then tax should be collected from the customer – any cabinetry and countertop installed in a non-kitchen or bathroom area, like in a doctor’s office or a work area room (paper copy station), bank teller stations, bars and food stations in restaurants, cashier counters, reception desks, and service desks and counters.

Call Marsu

Countertop manufacturers and installers are one of the most often audited types of businesses. That is because the MD sales tax law is so confusing and there are so little guidelines available. If you are a countertop manufacturer and installer and have been audited in the past, then please callMarsu now to determine if your case can be reopened pursuant to Section 13-509 of the Annotated Code of Maryland to get any taxes improperly assessed back as a refund or if you are just due a refund of sales and use taxes paid in error. Marsu’s review is performed on a contingent basis and no fee is due if no refund is approved by the Comptroller’s Office.

A three-year-old Company gets audited by the Comptroller’s Office for failure to collect sales tax on a taxable service – commercial window cleaning. Marsu was contacted by their accountant to assist their new client with the audit. The workpapers were just received by the Taxpayer so Marsu was able to perform the review of the workpapers in the field with the auditor. Like any other audit, the auditor reviewed a sample period of sales and expenses and projected the assessment over the 3 plus year audit period and reviewed all asset purchases. Marsu did the following for the three schedules:

For sales, the auditor reviewed six months of sales and listed the total commercial sales for each month as a separate line item on the schedule. The auditor also did list three exceptions as non-taxable sales on this schedule to calculate the taxable sales amount for the sample period. Marsu reviewed these sales and found 17 more exceptions that were approved. The tax assessed was reduced from $12,432.74 to $9,122.49, a savings of $3,310.25.

For expenses, the auditor reviewed six months of purchases and listed 12 line items as taxable. Marsu found no errors with the 12 lines listed but found that the projection schedule was incorrect in the fact the auditor did not use the total purchase amount for the accounts being audited for the sample period. Once corrected, the tax assessed was reduced from $2,698.91 to $397.05, a savings of $2,301.86.

For assets, the auditor listed 7 line items where use tax was not properly paid on out of state purchases. Marsu found no errors with this schedule.

Marsu was able to make one more adjustment to the assessment. Marsu discovered in the sales tax returns folder that the Taxpayer had filed a Combined Registration Application to collect sales tax but was denied by the Comptroller’s Office. The Comptroller’s Office had stated in their reply that commercial window cleaning was a service and tax did not need to be collected. I brought this to the attention of the Director of Compliance and the hearing officer abated the interest on the sales portion of the audit and all penalties.

Main Tax Issue

For fifty years, Maryland was a tangible state meaning that sales tax was only collected on the sale of tangible personal property. Effective July 1, 1992, that all changed when the Comptroller’s Office amended the law to include certain services as taxable services. Seems like whoever was processing the Combined Registration Applications missed that change and this Taxpayer paid the price. It cost him $10,008.55 and a lot of aggravation.